Credit Reports are basically a report that contains your credit history – both the good and bad. If you watch late-night TV, you have probably seen a few commercials offering free credit reports, so you might know that these are important. Most people, however, don’t know just how big a role a credit report can play.

What is a Credit Report?

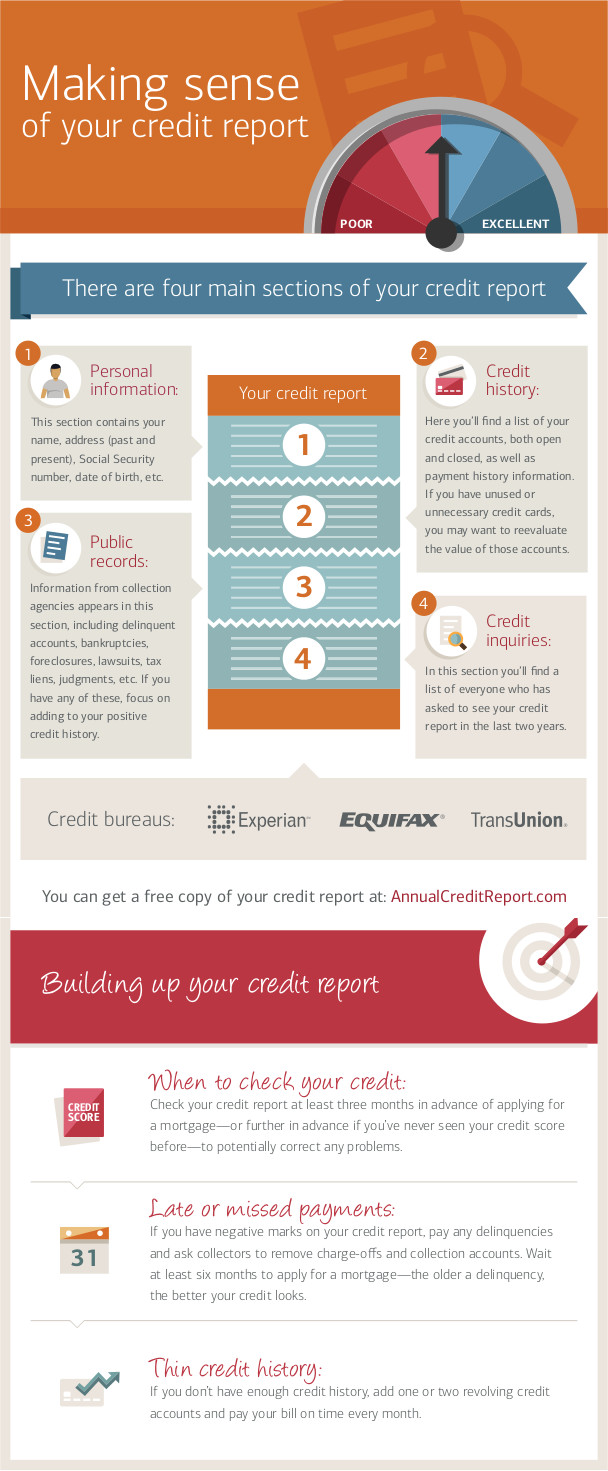

A credit report, at its core, is a document that keeps a record of (most) of your regular bill payments. There are three main organizations that provide credit reports in the United States: Experian, TransUnion, and Equifax.

Each of these organizations is specially licensed to collect information on all individuals in the US related to their credit and payment history, criminal record, bankruptcies, and lawsuits. Your “Credit Report” is basically your file that they have on all of these activities for the last 7-10 years.

Companies and organizations from whom you are requesting credit can then ask one of those 3 agencies for a copy of your credit report to help them assess your application for credit. This would include any time you want to open a credit card, take out a loan, get insurance, or renting a home. Sometimes even potential employers might request a copy of your credit report, although in this case you need to provide consent.

What is the difference between a “Credit Report” and a “Credit Score”?

Your credit report is a complete credit history, meaning the bills you have paid (or didn’t pay), and their amounts. A “Credit Score” is a single number.

Since a credit report can have a lot of different information from different sources, this is consolidated by using what is called the “FICO score”. The “FICO score” basically distills all your credit history down to a number – the bigger this number is, the more likely the credit agencies think you will pay your bills on time. If you have a clean credit report you will have a high credit score. On the other hand, if you have a poor credit score, you probably have a lot of late payments or complaints in your credit report.

Your income does not impact your credit score, but repeated requests to review your score do have a negative impact, since the credit rating agencies assume that if you are trying to get a lot of different credit from a lot of different places, your financial position might be unstable.

Why Do I Need To Care?

Your credit report, and credit score, are important, and can have a huge impact on your financial life. Anyone who would need to assess your financial trustworthiness will probably be looking at your credit report, so it is absolutely in your best interest to keep it looking good.

Applying For A Credit Card

The first time your credit report might come up is when you apply for a credit card. Based on the length credit history (meaning the total size of your credit report), your credit score, how well you have kept up with any previous payments, and your income, you will have a very wide range of credit options available.

Generally speaking, people with a poor credit history have lower spending limits, higher interest rates, and less likely to get any leeway with their credit card company with late payment forgiveness or credit card perks. On the other hand, if your credit report looks good, you will have a wide pick of different credit card companies offering increasingly attractive terms to attract your business.

Applying For A Mortgage

If your credit history is poor, you might have trouble securing funding for a home at all. When you want to buy a house, you will see the same kinds of terms as when you apply for a credit card, but with much higher stakes. This means more banks and lenders willing to lend to you in the first place, better interest rates (which can save you tens of thousands of dollars over the life of the loan), and more flexible down payments.

Renting an Apartment

When you rent an apartment, your potential landlord will probably look up your credit report. Renters often use the credit report to compare different candidates and determine the size of the security deposit. Remember – a person renting an apartment is primarily concerned with making sure the rent is paid on time. If you have a poor credit report, they might rather wait for the next applicant than take a risk.

Getting Insurance

While it might not play as large a role as direct lines of credit, insurers also look at your credit report when they determine your premiums and deductibles. This is because they want to make sure all of their clients are paying on time. The entire idea behind insurance is that the insurance provider is taking in at least as much money from premiums as they are paying out in claims, so they need to make sure all of their clients are paying their premiums on time.

If the insurance company suspects that you will lapse on your coverage, just to start catching up right before filing a claim, they will likely charge you higher premiums to make up for it.

Applying For A Job

More and more employers are requesting the credit history from potential job applicants. This trend first started in the finance and banking industry, but has been spreading to other sectors as well. Potential employers see your credit history as your overall professional trustworthiness, particularly if you have a long history of late payments.

What Exactly Is In My Report?

Your credit report follows your basic payment history to creditors. This includes:

- Credit Card Payments

- Cell Phone Payments

- Cable/Internet Payments

- In-Store Financing For Large Purchases

- Unpaid Parking Tickets

- If You Have Been Sued

- Any Other Outstanding Debt

- Mortgage Payments

- Rent

- Utilities (Gas, Phone, Water)

- Car Payments

- Unpaid Taxes

- If You Have Declared Bankruptcy

- Pay Day Loan Payments

Items in your credit report do not stay there forever, so even if you make credit mistakes when you are young, you might not need to suffer from them forever. Generally speaking, missed bill payments, collections, and most other items expire after 7 years. Bankruptcies and other civil judgments (like unpaid taxes) usually have a longer expiration, up to 10 years.

How Does This Information Get In My Credit Report?

Generally speaking, the more a company uses credit reports as part of their decision to do business with you, the more likely they are to provide information that will be included in future reports. The three credit reporting agencies get all of this information from your creditors, meaning everything in your report was given to them by someone you did business with (or sued you). Not every creditor supplies this information. For example, if you rent an apartment, the payments might not appear in your credit report unless your landlord makes a point to report it. This is sometimes unbalanced, since landlords might not always report timely payments (or even late payments), but almost certainly will report judgments and collections.

Your creditors report this information, which is linked to you through your Social Security Number and your address. The Social Security Number is the main way it is linked, but they address is also used to help prevent fraud and identity theft.

The Fair Credit Reporting Act

All of these details so far have been helpful for creditors and employers, but you also have some control over your credit report that comes from the Fair Credit Reporting Act. This is a law that gives all consumers certain rights to their credit report, along with restrictions on businesses on what they can include in the report (and how they can use that information).

Consumer Rights

The most fundamental right you have is that each person can get a free copy of their credit report from all 3 of the main agencies once per year. This is done through annualcreditreport.com. Once you have your credit report, you can also dispute any claims on it if you feel they are not legitimate. This means you can call the agency who provided the report and file a “dispute”. You also need to contact the lender who made the report to ask them to issue a correction if it is inaccurate. If the claim was because of an error, it will be removed from your report.

Even if a claim is not an error, you can contact the business who filed the claim and try to get it removed – if the person who files the claim withdraws it, it also is removed from your report. This is most often the case when people move out of their home without paying the final utility bills. If you contact the utility company and pay the outstanding bills (plus a fee), they may withdraw the claim entirely from your report. If you do have any such claims, it is always in your best interest to find them and take care of them as soon as possible, since it will impact your overall ability to obtain credit. For more information on disputing claims, visit http://consumer.ftc.gov.

If a potential employer wants to see your credit report, they need to get your written permission, only use it for the purposes of hiring you (and tell you what those exact purposes are), give you a copy of the report if they decide not to hire you (or fire you), and give you an opportunity to dispute any outstanding claims before they make their final decision.

If you get denied credit (or a job) because of the contents of your credit report, you also have the right to get a free copy for your own reference.

User Responsibilities

Businesses who order credit reports also have limits on how they use them. Generally speaking, a business who orders a credit report must:

- Only use the report for deciding the terms of your financial agreement

- Notify someone if something in their credit report affected their final decision

- Tell the consumer which company they got the report from so the consumer can verify it.

Data Provider Responsibilities

People and businesses who provide the data that is included in credit reports also have their own responsibilities. The most important of which is to make sure all the information they report is accurate and up-to-date.

This means that if you file a dispute, the data provider has 30 days to verify that the claim is accurate, or else it is removed from your report until they do so. The data provider must also take some safeguards to prevent against data theft. This is why they require both a social security number and an address, so these items can be cross-referenced to check for identity theft.

The data providers also need to tell consumers before they file a claim and give them a chance to resolve it before it appears on their credit report.

Fixing Mistakes

Watch this great video from Bank of America showing how to find mistakes on your credit report, and get them corrected.

The Bottom Line

Your credit report is important, so don’t forget about it. You get one free look at your credit report each year (note – this report does NOT include your credit score), so you should take advantage of it. Some studies have shown that up to 30% of credit reports have some inaccurate information, and it is always in your best interest to have these resolved as soon as possible.

Junk Bonds

Junk Bonds How to justify your Forex trading performance?

How to justify your Forex trading performance?